Dutech Holdings Ltd is engaged in the design and manufacture of ATM safes, fire-resistant commercial safes, safes for storage of weapons, and other security products. The Company also provides business solutions to customers. It has a strong economic moat which is intangible assets due to patents is required for safety and security products and also efficient scale due to only small market is producing safety and security products.

This stock is consider good bacause it has consistent Earnings Per Share (EPS), has positive Operating Cash Flow for the past 10 years and has Debt/Equity of 0.01 (< 0.5) in the last year and also the Return of Equity (ROE) is more than 15% most of the years.

Besides, the Price/Earning (PE) is 4.7 (<12), Price/Book (PB) is 0.6 (has 40% discount) and Dividend Yield % is 5.9%.

This stock would suffer regulatory risk due to safety and security products are highly regulated by government and also science and tech risk due constant R&D is needed to improve on the safety and security products.

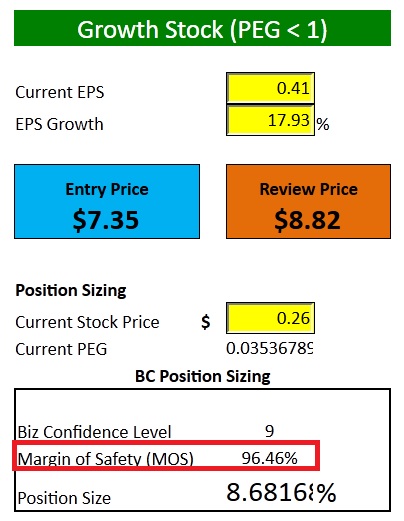

The current price for this stock is SGD0.26. From stock valuation, the

biz confidence level is 9 out 10, can buy it now as growth stock

because its PEG<1, the current price is lower than entry price (SGD7.35) and has

margin of safety (MOS) of 96.46%.

Can buy it now as dividends stock also

because the current price (SGD0.26) is lower than entry price (SGD1.00) and has positive margin

of safety (MOS) of 74%.

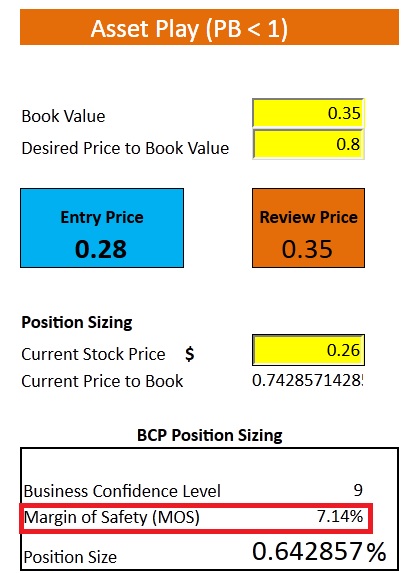

Can buy it now as asset play stock also

because the current price (SGD0.26) is lower than entry price (SGD0.28) and has positive margin

of safety (MOS) of 7.14%.

Hey David! You have a great value investing blog. Just want to check what software do you use?

ReplyDelete