Lee Metal Group Ltd is the distributor & fabricator of steel products & a recognized international trader of steel and steel related products. The Company is engaged in business segments: Steel Merchandising and Fabrication & Manufacturing. It has a single economic moat which is cost advantage due to its business has international market presence which give it the benefits of better position in pricing to stay competitive.

This stock is consider good bacause it has quite consistent Earnings Per Share (EPS), has positive Operating Cash Flow for 9 years out of 10 years in the history, has Debt/Equity of 0.1 (< 0.5) in the last year and also the Return of Equity (ROE) is more than 15%.

Besides, the Price/Earning (PE) is 8.1 (<12), Price/Book (PB) is 0.8 (has 20% discount) and Dividend Yield % is 6.9%.

This stock unlikely would suffer from any of the risks (regulatory, inflation, science&tech or key people).

The current price for this stock is SGD0.29. From stock valuation, the

biz confidence level is 9 out 10, can buy it now as dividends stock because the current price is lower than entry price (SGD0.40) and has positive margin

of safety (MOS) of 27.5%.

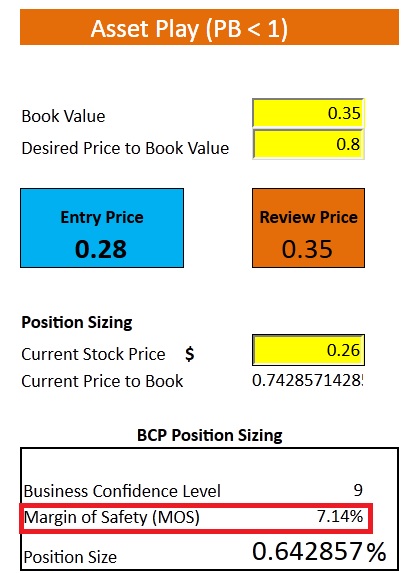

Can buy it now as asset play stock also because the current price (SGD0.29) is lower than entry price (SGD0.30) and has margin of safety (MOS) of 2.03%.

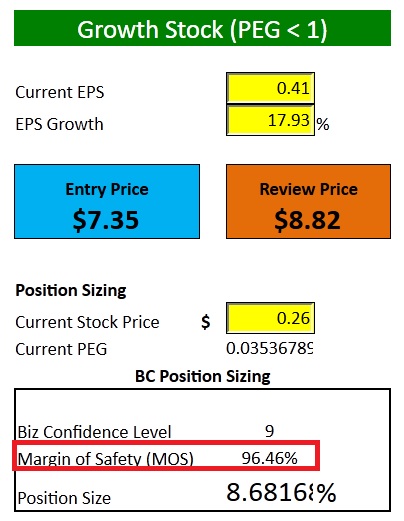

This stock is not suitable to buy as growth stock at the moment because the current price (SGD0.29) is a bit higher than entry price (SGD0.26) and has negative margin of safety (MOS) of -9.89%. It can buy as growth stock when the stock price falls below SGD0.26 and has positive MOS.